MALKIEL, Burton G.

The Journal of Portfolio Management: The Structure of Closed-End Fund Discounts Revisited.

New York: Institutional Investor, Inc. , 1995.

$975.00

In Stock

Item Number: RRB-152014

+$450

Facsimile Offprint of the Summer 1995 Issue of The Journal of Portfolio Management, Containing Burton Malkiel's "The Structure of Closed-End Fund Discounts Revisited"; Signed by Him and From His Own Personal Collection

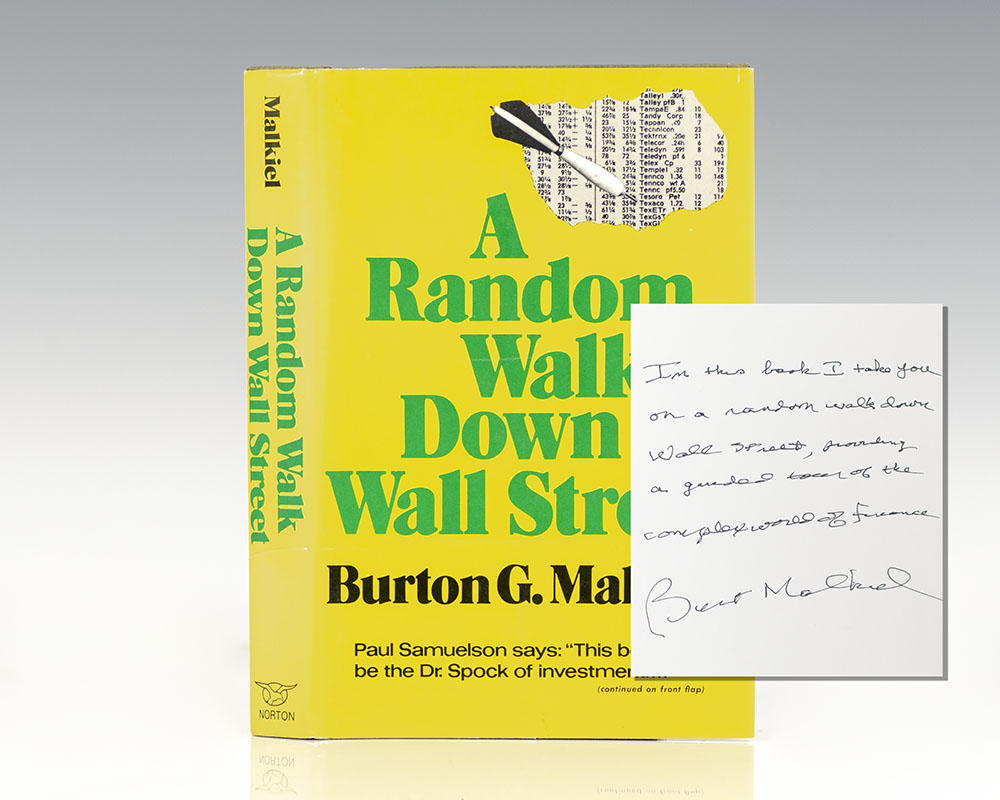

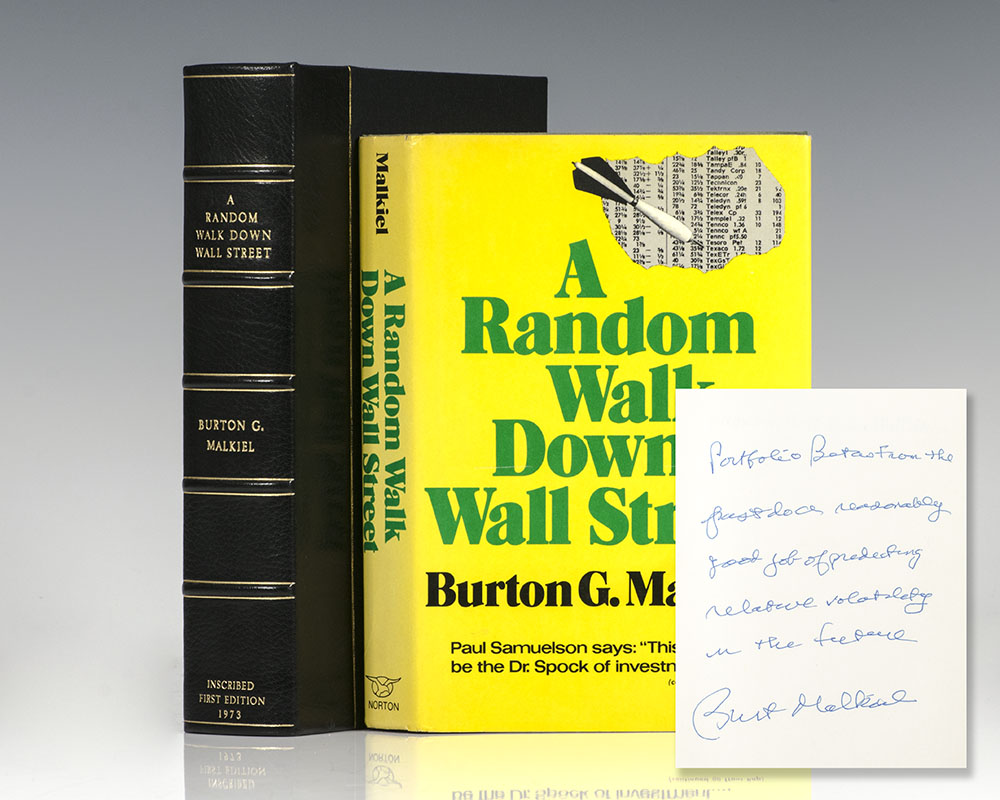

Facsimile offprint of the Summer 1995 issue of The Journal of Portfolio Management, containing Burton Malkiel's article "The Structure of Closed-End Fund Discounts Revisited", from his library. Octavo, original wrappers, volume 21 number 4. Boldly signed by Burton Malkiel on the front wrapper. Burton Gordon Malkiel is one of the most consequential financial economists of the postwar American academy, whose career as scholar, institutional leader, and public intellectual has made him a central figure at the intersection of investment theory, market efficiency, and public policy. Educated at Harvard and Princeton, where he spent the most productive decades of his career as Chemical Bank Chairman’s Professor of Economics, Malkiel also served as Dean of the Yale School of Management from 1981 to 1988 and as a member of the President’s Council of Economic Advisers under Gerald Ford from 1975 to 1977. His scholarly output encompasses foundational contributions across the term structure of interest rates, convertible security valuation, corporate capital structure, closed-end fund discounts, mutual fund performance, and gender pay differentials in professional employment, producing a body of work whose empirical breadth places him among the most versatile financial economists of his generation. His long service on the board of directors of The Vanguard Group connects his academic advocacy for passive investing to the institutional infrastructure that has most fully realized it in practice. It is nevertheless A Random Walk Down Wall Street, first published in 1973 and now in its thirteenth edition, that secured his place in the broader culture: a work of lucid, empirically grounded argument for market efficiency and index fund investing that has sold over 1.5 million copies and permanently altered the investment behavior of millions of individual investors worldwide. From the personal library of Burton Malkiel. In near fine condition.

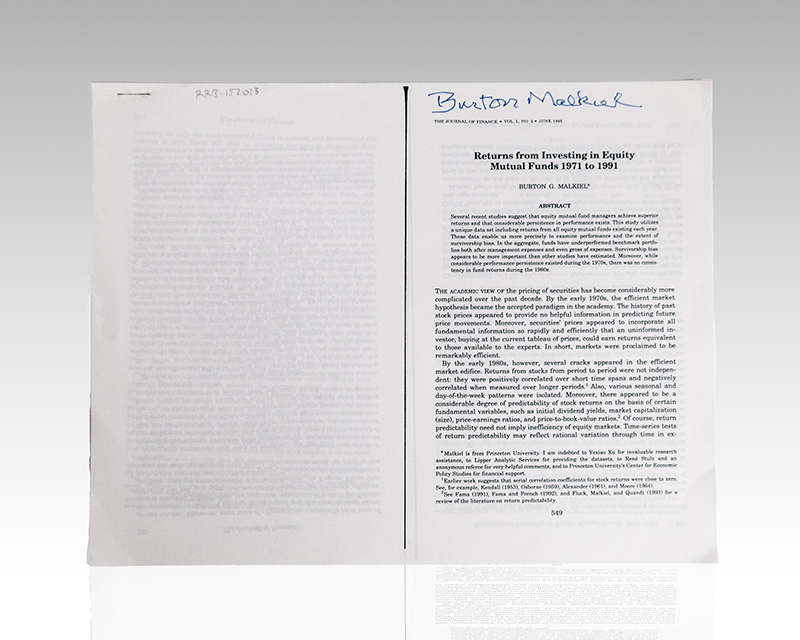

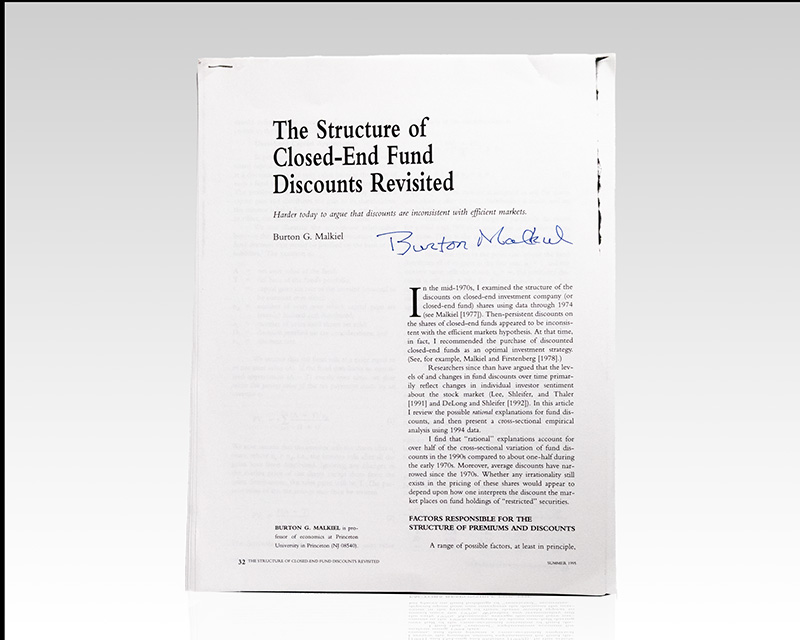

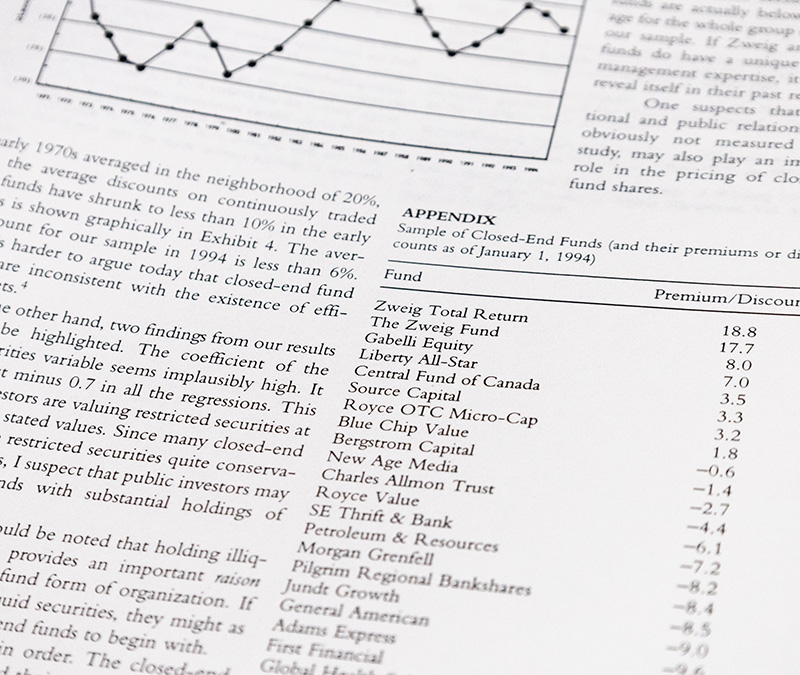

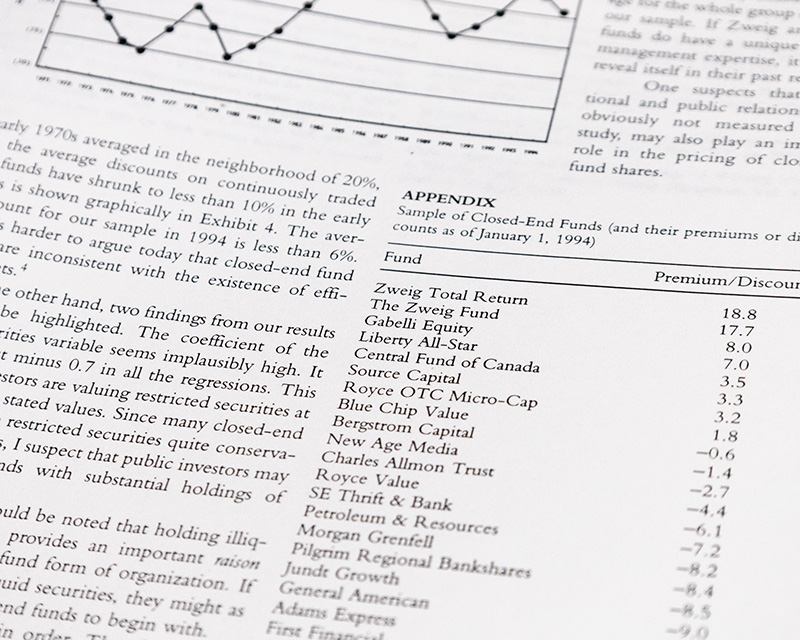

"The Structure of Closed-End Fund Discounts Revisited," published in The Journal of Portfolio Management, Volume 21, Number 4, Summer 1995, is a significant contribution to one of the most persistently debated puzzles in financial economics, extending and updating a line of inquiry that Burton G. Malkiel had opened nearly two decades earlier with his foundational 1977 paper "The Valuation of Closed-End Investment-Company Shares," published in The Journal of Finance. The closed-end fund discount puzzle refers to the well-documented phenomenon whereby shares of closed-end funds trade in the secondary market at prices that differ, often substantially and persistently, from the net asset value of the underlying portfolio — a state of affairs that poses a direct challenge to simple notions of market efficiency and rational pricing. Malkiel's 1977 paper had examined the structural determinants of these discounts and premiums, finding that unrealized capital appreciation, portfolio turnover, management expense ratios, and the proportion of assets invested in restricted securities all contributed to the observed pricing behavior. The 1995 paper revisits that framework in light of the subsequent literature, which had grown substantially to include the celebrated behavioral finance interpretation advanced by Lee, Shleifer, and Thaler in their 1991 paper attributing closed-end fund discounts to fluctuations in individual investor sentiment rather than to rational assessments of fund-specific characteristics.

The Journal of Portfolio Management: The Structure of Closed-End Fund Discounts Revisited.

$975.00

In Stock

Other Books by this Author